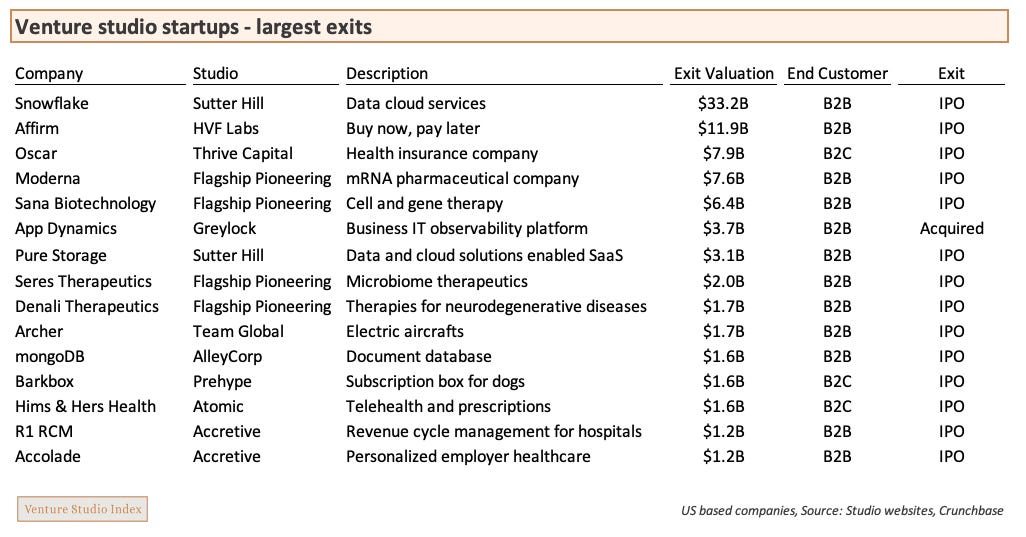

The largest venture studio exits

What do the most successful venture studio startups have in common?

Welcome to Venture Studio Index - data and research on the venture studio industry. If you aren’t subscribed, join the hundreds of studio executives, EIRs and future founders reading each week:

I analyzed 1,700+ venture studio startups to learn what the most successful ones have in common.

Key takeaways

Most exits are in B2B verticals such as data, biotech and healthcare

Most exits are via acquisition but all the biggest outcomes are IPOs

Most of the winners were launched by studios or incubated by VCs who manage large funds, and who also invest in external startups

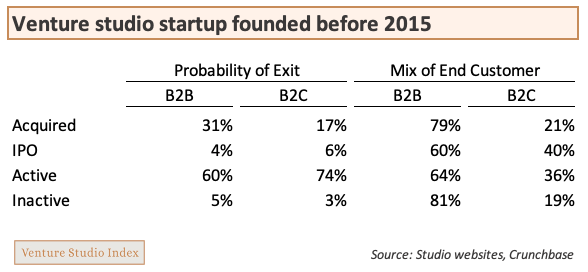

The probability of a successful exit is 35% for B2B startups and 23% for B2C startups

The data

The above table covers venture studio startups operating for at least 7 years, broken out by exit status and business model. While most startups are still private, ~30% have either IPOed or been acquired.

Most studio startups are B2B, and B2B startups have a significantly higher probability to be acquired. Consumer startups have higher, but still low, probability of IPO.

The chart above lists the largest U.S. based exits, which almost entirely occurred via IPO. The sole M&A exit, App Dynamics, was acquired by Cisco right before it went public.

The primary verticals are data, biotech and healthcare.

Methodology and data limitations

Startup and studio data comes from our database of venture studios and their startups. See data methodology and limitations for more background.

Probability of exit for startups launched after 2015 in the first chart is derived by the number of startups in each status divided by all startups.

Exit valuation is the market cap of companies upon IPO or the purchase price upon acquisition. This analysis is focused on exits and excludes large companies who are still private but may have already afforded studios opportunities to sell secondary - as the data is not publicly available.

Exit valuations are found via Crunchbase and public trading statistics. While exit valuation is a good proxy for economic return to the studio, it does not factor in dilution from subsequent fundraising rounds, secondary sales before exit, when the studio was able to sell following an IPO, among other factors.

Certain IPOs, particularly B2C companies, experienced significant share price declines immediately following IPO.

This analysis focuses on U.S. based companies to illustrate business models and industries that tend to produce successful outcomes. It excludes notable global studio startup exits such as Global Fashion Group, Delivery Hero and Home24, which often replicate US based consumer business models overseas.

Conclusion

While the majority of successful exits are via M&A, the biggest winners go public.

Many of the largest winners were created by studios or incubated by VCs managing large funds - e.g., Sutter Hill, Greylock, AlleyCorp, Thrive Capital - who do significant external investing as well as in-house builds.

The institutional LP base for traditional VC investing is much larger than for venture studios, enabling firms with a VC practice to raise accordingly larger funds, part of which can be allocated to in-house builds.

Access to capital is particularly strategic here given the largest startup outcomes are B2B companies in deeply technical and/or regulated fields such as data, biotech and healthcare. These startups require large investments in R&D and customer pilots before gaining traction. This gives firms managing larger funds an advantage.

Given their strategic advantage here, we may see more VC firms to pursue incubations.

I also expect studios to raise increasingly larger funds enabling them to make larger investments in their startups pre-launch. LP interest in this emerging asset class should continue to grow given the high average success rate and numerous large outcomes outlined above.